The Fiscal Singularity

The Baseline? Financial Repression. The Optimal Asymmetric Hedge? Bitcoin.

Executive Summary

The United States faces a fiscal singularity. Structural deficits, positive real rates, and competing borrowing needs from AI infrastructure drive exponential debt growth under current policy.

The baseline outcome—financial repression with periodic liquidity expansion and inflation bursts—carries the highest probability (around 80–85%). Lower-probability tails include marginal stabilization through acute pain-forced reforms or an AI productivity miracle.

Escape remains unlikely without politically untenable changes. Policy incentives (stablecoin Treasury demand, Strategic Bitcoin Reserve, controlled USD devaluation) synergize to extend the system while exporting some inflation to scarce assets.

Bitcoin uniquely serves as a global release valve, absorbing excess liquidity without harming essentials, defending against AI cyber threats via proof of work, and compensating savers in a debasement regime.

Financialization introduces near-term volatility but builds long-term legitimacy and depth. This creates textbook asymmetry.

In light of these realities, Bitcoin stands as the optimal hedge and purest expression of global liquidity for those with conviction and resilience.

The full essay explores the math, timelines, AI bimodality, incentives, and falsification criteria in detail.

The Inescapable Math

Over the next 5 to 10 years, AI and the US Treasury both need to borrow trillions. Positive real rates create powerful exponential pressure on the debt. AI’s trillions in borrowing produce a fat-tailed, bimodal fiscal outcome that could accelerate or partially offset the spiral depending on productivity and tax-receipt results.

Uncertainty bands remain wide, but the structural pressures stay directionally clear. The fiscal trajectory leans unstable absent meaningful and highly unpalatable policy change.

High rates widen the structural fiscal deficit. Low rates spur speculative attacks on fiat through borrowing dollars to buy hard assets such as Bitcoin.

Under current policy and politics, a long-term fiscal spiral is the highest-probability baseline by the 2030s.

Lower-probability tails exist for marginal stabilization via some combination of entitlement indexing tweaks, immigration-driven labor-force growth, and AI-driven revenue surprises once interest pain becomes acute enough. These probabilities are grounded in historical precedent for policy inertia and delayed reform.

Debt dynamics follow this equation:

d_(t+1) = d_t × (1 + r − g) + pd

Current inputs lock in exponential growth:

Debt held by the public at 2025 starts at 100% of GDP.

Real rate (r) ranges from 2% to 2.5%.

Real growth (g) ranges from 1.7 to 1.9%.

Primary deficit (pd) ranges from 2.5 to 3% of GDP.

This yields an r − g spread of +0.6 to +0.8%, with positive primary deficit, leading to exponential growth in the baseline scenario.

These inputs align with CBO, Treasury, and market pricing. The long-run r–g spread remains uncertain. Even modest shifts substantially alter the trajectory. Tail scenarios incorporate this uncertainty explicitly.

Escape Routes and the AI Wildcard

A large primary surplus or +50% tax hikes carry near-zero probability today. Sustained growth above 4% carries less than a 10% chance.

Marginal 0.5 to 1.0% of GDP primary-deficit improvement via indexing, immigration, or AI revenue surprises carries a 15 to 25% probability once interest hits 5 to 6% of federal revenue. This is the pain threshold that forced 1983, 1990, 1993, and 2013 reforms.

Aging demographics amplify entitlement pressure, and the 65+ population share will rise to a projected 23% (2040), further constraining reform options.

Structural entitlements, population trends, AI disruption, and concomitantly record high public and private debt coincide to render the debt deleveraging of the 1940s and 1970s infeasible.

AI infrastructure buildout is short-term inflationary and tax-positive. Post-2028, however, the outcome is bimodal:

The probability of net tax-base erosion (labor displacement dominates) is slightly higher than the probability of net tax-base expansion (productivity leads to corporate profits, capital gains, and new sectors).

Either way, borrowing competition keeps upward pressure on rates and favors fiscal dominance as the path of least resistance.

The key uncertainty is distributional: Who captures the productivity gains, and how much is taxable?

Money borrowed for AI goes into GPUs, data centers, and electricity infrastructure, much of it depreciated quickly or not labor-intensive. AI replaces human labor at scale (white-collar knowledge work first).

This yields massive productivity gains but plunging employment and wage growth. Fewer income and payroll taxes follow, along with higher unemployment benefits, lower consumer spending, and shrinking tax receipts for the Treasury.

In extreme scenarios, AI-driven job displacement could cause trillions in consumer/household debt defaults (mortgages, auto loans, credit cards) when people lose jobs en masse, forcing the Fed to bail out the system again.

AI infrastructure buildout and development is short-term inflationary, creates jobs, and has driven much of 2025's GDP growth. Tax revenue from that growth and investment is significant but does not meaningfully change the fiscal trajectory absent an unlikely productivity miracle.

Immense borrowing for AI CapEx and Treasury puts upward pressure on rates as the Fed seeks to lower them. AI can be deflationary for unit costs of certain goods/services (software-driven productivity) too, of course.

A debt-based financial system requires rising nominal incomes and credit expansion so lenders are paid back in nominal terms. If AI lowers prices but concentrates income in capital owners (much of which is sheltered or invested offshore), then real GDP may rise while taxable nominal receipts stagnate or shift.

This fails to relieve sovereign nominal obligations.

Deflation increases the real value of debt, making servicing harder and incentivizing monetization or debt restructuring. AI’s deflationary effects are not a natural counterweight and often complicate fiscal stress, especially in an unprecedented era of digital abundance that introduces a novel set of problems solved only by digital scarcity.

AI and Bitcoin Synergize

Bitcoin’s proof of work system secures the network by imposing irreducible real-world energy costs on transaction validation. As AI-driven cyber capabilities scale and computational costs collapse, purely logic-based defenses become increasingly fragile.

Proof of work introduces a physical cost function that autonomous systems cannot bypass cheaply or at scale, making it a structurally robust security primitive in an AI-rich world.

This property positions Bitcoin not only as a debasement hedge, but as a digitally scarce asset with unique resilience characteristics. If AI-driven automation expands attack surfaces faster than institutions can defend them, then Bitcoin’s security model becomes incrementally more valuable.

Beyond security, AI will likely expand Bitcoin’s utility:

Microtransactions: Bitcoin’s divisibility down to 1 satoshi enables machine-to-machine payments.

Autonomous agents: AI systems can transact natively without intermediaries.

Neutral settlement layer: Bitcoin functions independently of jurisdiction or platform control.

Bitcoin provides the trustless financial infrastructure, offering decentralization, security, and global accessibility. AI brings intelligence and automation, enabling smarter and more efficient use of Bitcoin’s capabilities.

Deflationary and digital technologies—AI centralizing, BTC decentralizing—form a symbiotic relationship.

Together, they can power a future of autonomous economies, decentralized governance, and seamless global transactions: The Internet of Money.

Although nascent, the trajectory of Andreas Antonopoulos's Internet of Money thesis since its release in 2016 points to validation rather than speculation. The proof of concept for AI Bitcoin synergies is strengthened by Layer 2 infrastructure advancements accelerating in parallel with the development of AI agents and LLMs and, as is the case with exponential technologies, progress is also nonlinear.

These use cases remain exploratory and supplementary to its role as digital gold. Nonetheless, they plausibly accelerate adoption asymmetrically and further cement Bitcoin's global importance as digital scarcity in an era of digital abundance.

The Spiral Timeline and Market Vulnerabilities

CBO states no currently plausible policy combination stabilizes debt. History shows pain may eventually force novel plausible options. Key tax cuts from TCJA just renewed. Entrenched entitlement spending and political gridlock persist.

The most plausible long-run path remains debasement, financial repression, or stealth monetization rather than broad, painful tax hikes or spending cuts. Tariff revenue is substantial but proves insignificant relative to multi-trillion deficits.

This outcome is not deterministic. Politics can surprise in both directions. With that said, the burden of proof rests on stabilization, not deterioration.

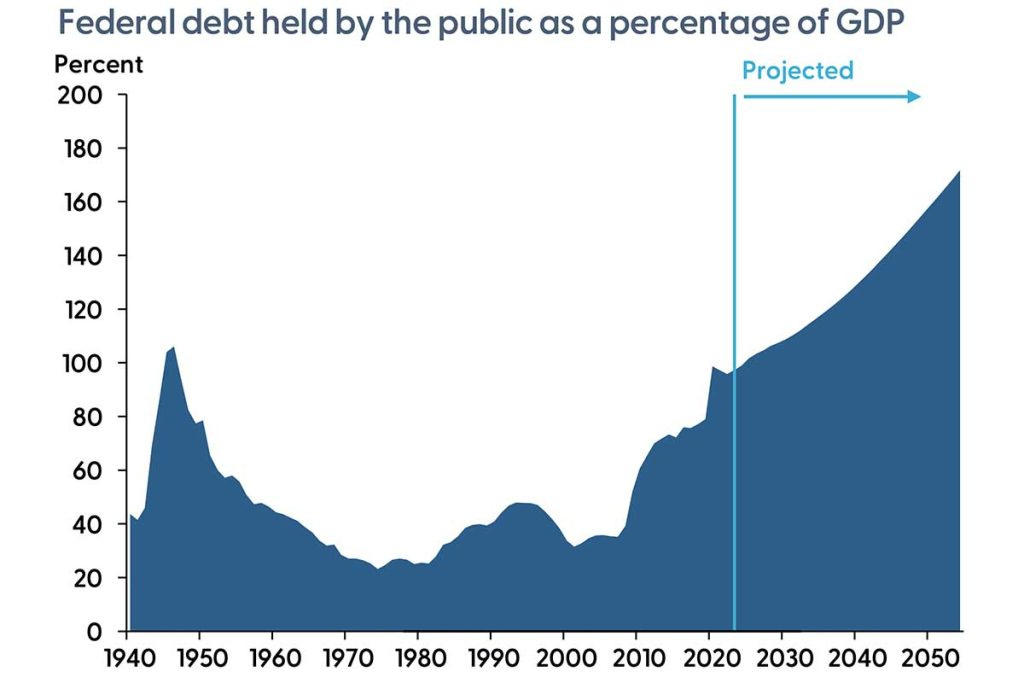

Under current policy:

2025: 100% debt-to-GDP

2030: 118%

2032: around 130%

2035: around 150% (exponential phase clearly visible)

2040: around 180 to 200% (acute crisis risk in baseline)

These figures reflect CBO long-run mechanics using conservative and optimistic assumptions. Actual outcomes vary with interest rates, real growth, geopolitical shocks, and policy responses.

Permanence of TCJA cuts removes a plausible reform upside path that skeptics point to. Bloomberg Economics’ million-simulation work shows 88% are unsustainable. GAO simulations project debt rising further absent policy change (106% by 2027 in their simulation, longer-run 200% by 2047 under current policy assumptions).

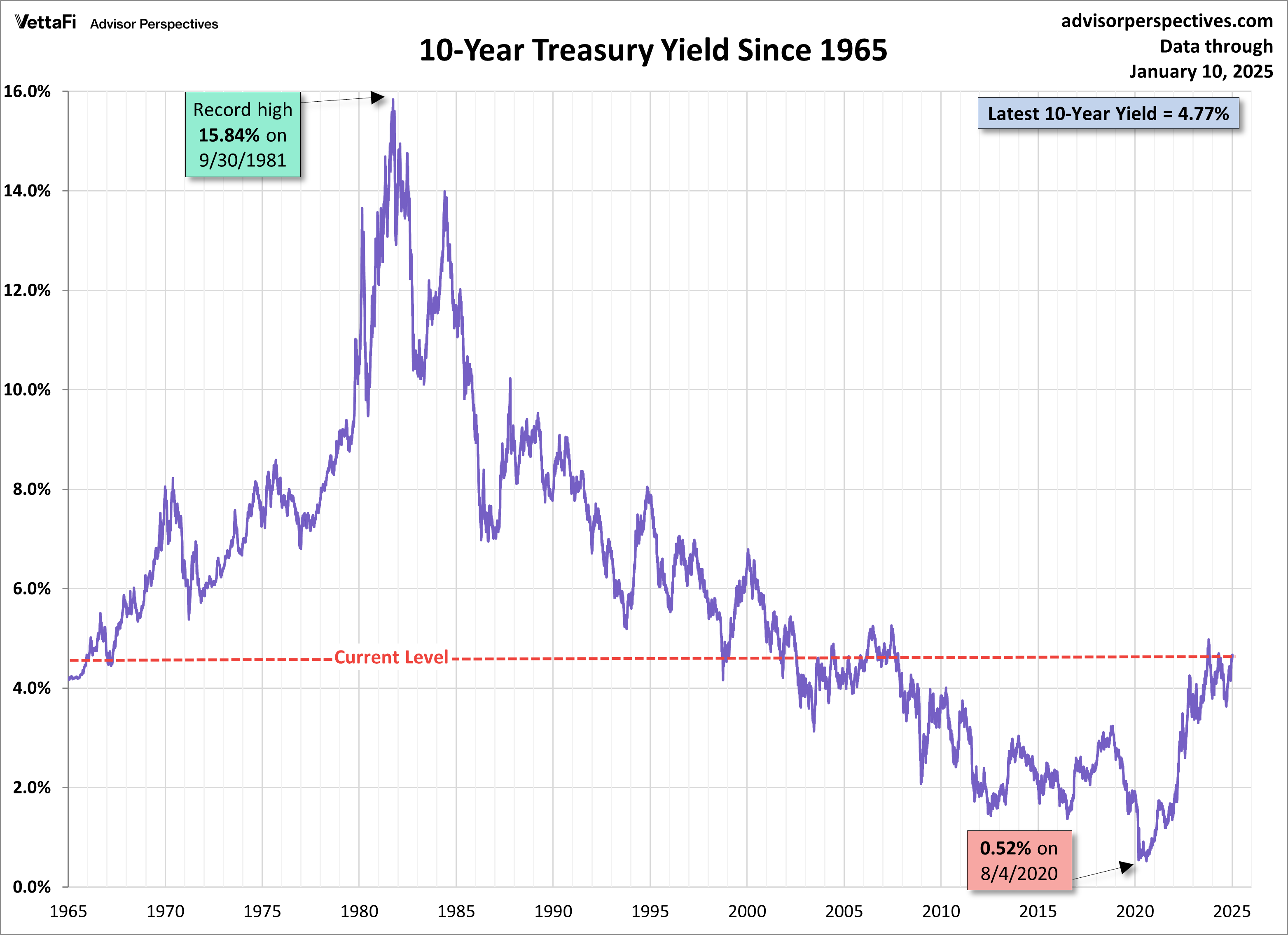

The 10-year yield remains around 4.1-4.2%. Foreign buyers hold down from 50% to less than 35% of Treasuries. TIC data shows China was the largest net seller of Treasuries in 2025, and they have reduced their holdings from $1.3T (2013) to ~$689B (2025), a nearly 50% decline. Confidence cracks remain the key upside trigger for yields.

A funding shock is not guaranteed, but the structural shift in global reserve allocations toward multipolarity increases vulnerability, especially during periods of fiscal stress.

Highest-Probability Outcomes

Monetary repression plus periodic balance-sheet expansion leads to chronic 4 to 8% inflation bursts and negative real yields. Attempted austerity or sharp yield spikes prove short-lived and politically reversed.

Outcome A is far more likely. Nevertheless, both outcomes favor hard assets.

Although the magnitude and timing remain uncertain, the directional bias toward financial repression matters.

Policy Incentives and Bitcoin as the Release Valve

The Trump administration's focus on expanding US Dollar stablecoins serves to increase US Treasury demand and support USD reserve system dominance.

Lower rates decrease net interest expense and, in turn, the deficit, ceteris paribus. On net, stablecoin demand and Bitcoin demand are positively correlated as well.

The weaker USD does not conflict with reserve strength longer-term because it serves to reduce the debt burden, decrease the trade deficit, and incentivize reshoring. A stronger USD would ironically hasten the debt spiral by making it harder to pay off.

Dollar devaluation is necessary to inflate away the debt (soft default). Stablecoin growth contributes to both USD devaluation against Bitcoin and the export of some USD inflation into Bitcoin; stablecoin minting mirrors fiat printing.

Recent policy developments suggest a structural shift toward Bitcoin integration. The establishment of the Strategic Bitcoin Reserve via Executive Order, alongside legislative progress including the GENIUS Act (signed July 18, 2025), the BITCOIN Act, and the Anti-CBDC Surveillance State Act (passed House July 2025), represent a fundamental policy pivot toward parallel monetary systems rather than adversarial regulation.

With the establishment of a Strategic Bitcoin Reserve, the US government promotes Bitcoin as a global reserve asset. If game theory plays out and Bitcoin’s price rises substantially, then its function as a repository for excess liquidity in the global financial system will likely grow in importance.

This reduces inflationary pressure on the real economy and commodities. Unlike tangible goods such as food or oil, Bitcoin price inflation does not directly harm consumers. It acts as a release valve because of this, absorbing some speculative capital that might otherwise flow into goods, services, or real assets.

As the USD inflates via stablecoin expansion, the real burden of debt (denominated in USD) shrinks. Meanwhile, Bitcoin’s rise compensates investors and savers, both institutional and retail, who might have otherwise lost wealth due to dollar devaluation.

This inverse relationship of abundant fiat and scarce Bitcoin uniquely addresses the structural wealth inequality inherent in fiat monetary systems. The Cantillon Effect ensures that those closest to the money creation process (banks, government contractors, asset holders) benefit from new money before prices rise, while wage earners experience the costs after inflation has spread through the economy.

By operating on a fixed supply with no central issuer, Bitcoin eliminates this structural asymmetry. Wealth accumulation becomes tied to productivity and time preference rather than proximity to the monetary spigot, creating a more equitable foundation for economic coordination that directly addresses rising anti-capitalist economic populism in the US and around the world in a positive-sum way.

Bitcoin is uniquely suitable for these roles and an N of 1 because:

Its supply is fixed (21 million coins), so its price can theoretically rise indefinitely to absorb excess liquidity.

It operates globally and can attract capital from outside the US, especially indirectly via stablecoins.

These pro-Bitcoin and pro-stablecoin policies, trade policies that have led to a weaker dollar, demands for lower rates, and DOGE-led (though largely futile) efforts to reduce the deficit are the economically and politically synergistic outcomes of aligned incentives.

Why Bitcoin?

Banks are chiefly leveraged bond funds in fiscal dominance. The highest-conviction place to store savings continues to be outside fiat-denominated, duration-exposed assets.

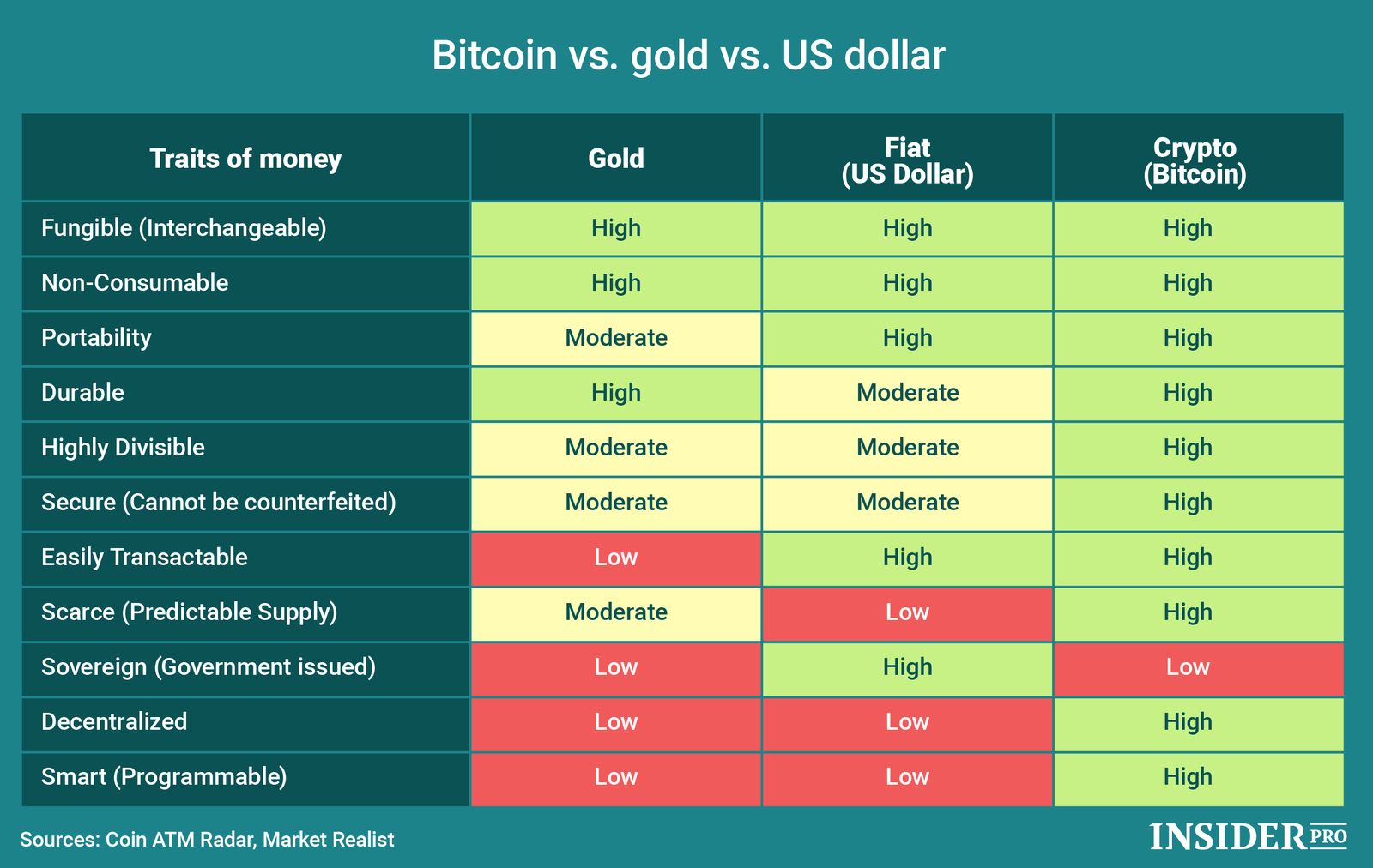

Gold remains viable but inferior in that it lacks Bitcoin's supply inelasticity (~1.5-2% annual gold production vs. zero Bitcoin inflation post-2140 and Bitcoin's now superior stock-to-flow), borderless transferability, ease of auditability, and game-theoretic reflexivity.

Bitcoin’s political tailwinds (ETFs, Strategic Reserve, state adoption) are powerful today but remain policy-dependent. There is a low but material 15 to 25% probability of reversal over a decade.

In the near-term, financialization legitimizes Bitcoin in the eyes of skeptics but temporarily amplifies volatility. Volatility delegitimizes Bitcoin in the eyes of skeptics and delays the market cap growth that would sufficiently dampen volatility. This creates a textbook asymmetric opportunity.

Purists lament that financialization corrupts by turning money into a casino. The core protocol remains unchanged, however, and self-custody, HODLing, and running nodes remain not only possible, but increasingly accessible as well.

Financial layers are optional on-ramps. More holders means stronger network security, higher hash rate, and unbreakable scarcity. This maturation brings capital, legitimacy, and volatility-dampening depth, driving price far beyond a spot-only trajectory.

While counter to its cypherpunk ethos, financialization is an inevitable outcome of Bitcoin's success and another long-term net-positive structural tailwind.

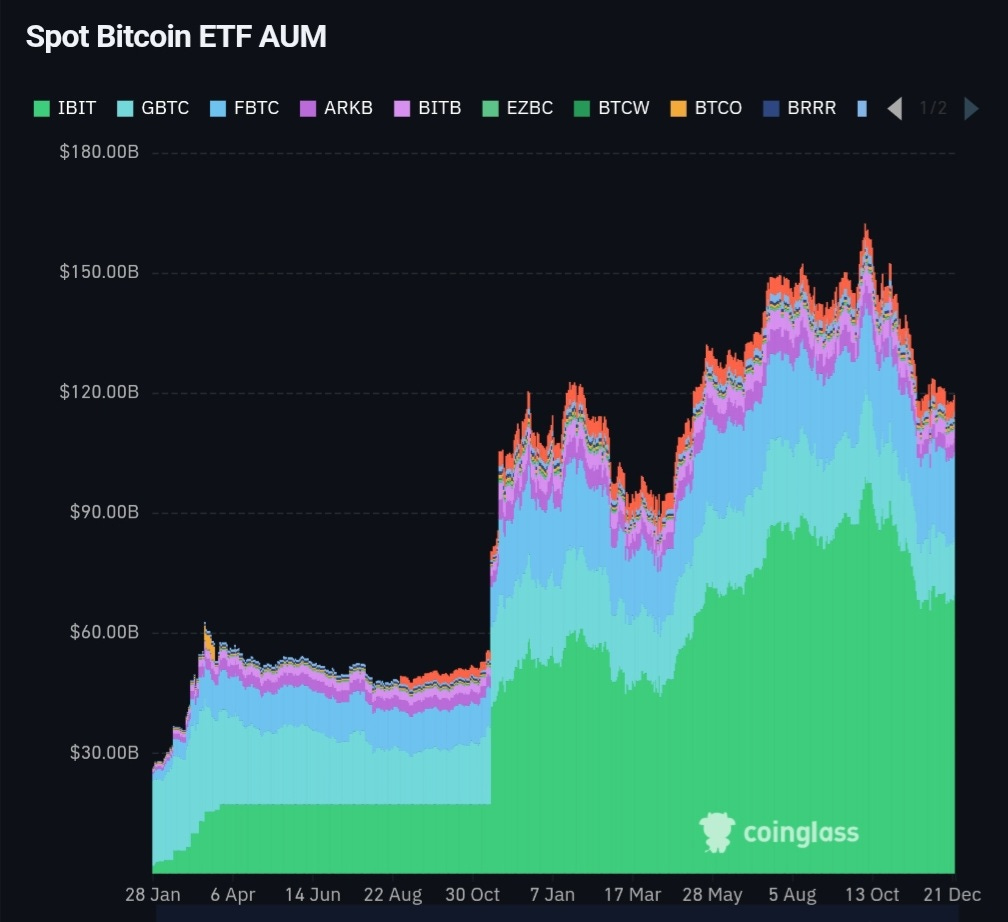

The Fed ended their QT program on December 1, 2025. Repo stress and reserve scarcity prime balance-sheet expansion in 2026. Liquidity is incoming and will ultimately be structurally larger than in 2019–2020. Same trigger, bigger outcome in the baseline scenario.

Unlike 2019-2020, the infrastructure underpinning tradfi access is now here.

Bitcoin is and will remain pristine collateral in the highest-probability debasement supercycle.

Thesis-Falsification Dashboard

The Fiscal Singularity Thesis loses validity if:

1. 10-year real yield falls and stays below 0.5% for 24+ months without balance sheet expansion.

2. Primary deficit drops below 2% of GDP for two consecutive fiscal years via legislation.

3. CBO 10-year debt-to-GDP forecast is revised downward by more than 20 percentage points in a single update.

These conditions are deliberately stringent but observable.

The system is heavily biased toward debasement.

My thesis assigns probabilities, not certainties, and remains open to falsification.

The Upshot

The Fiscal Singularity thesis is probabilistic, falsifiable, and grounded in structural pressures rather than deterministic collapse narratives.

The case for hard-asset positioning rests on relative asymmetry, not absolute certainty. Nevertheless, in light of structural fiscal realities, policy dynamics, and impending AI risks, Bitcoin is the purest expression of global liquidity and the optimal asymmetric hedge.